Auto insurance is a contract between you and an insurance company that provides financial protection in the event of an accident, theft, or other covered incidents. It typically consists of different types of coverage, each serving a specific purpose.

Tip 1: Know Your State’s Minimum Requirements:

Auto insurance requirements vary by state, so it’s essential to know the minimum coverage mandated by your state’s laws. Common types of required coverage include liability insurance, which covers injuries and property damage you cause to others.

Tip 2: Evaluate Your Driving Habits:

Consider your driving habits and the level of risk you’re comfortable with. If you have a long daily commute or frequently drive in high-traffic areas, you may want to opt for more comprehensive coverage to protect against potential accidents.

Tip 3: Understand Types of Auto Insurance Coverage:

Liability Insurance: Covers injuries and property damage you cause to others. It’s often split into bodily injury liability and property damage liability.

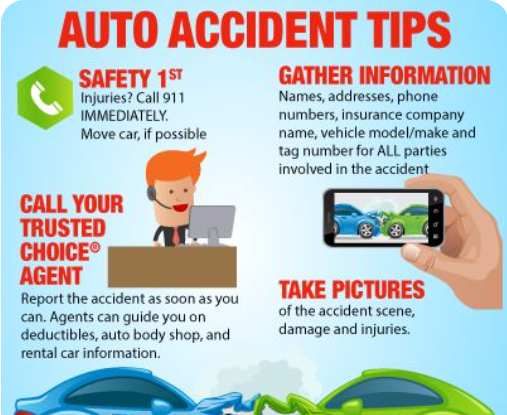

Collision Coverage: Pays for repairs to your vehicle after a collision, regardless of fault.

Comprehensive Coverage: Covers non-collision incidents such as theft, vandalism, or natural disasters.

Uninsured/Underinsured Motorist Coverage: Protects you if the at-fault party doesn’t have insurance or has insufficient coverage.

Tip 4: Consider Your Vehicle’s Value:

The value of your vehicle influences the type and amount of coverage you may need. If you have a new or high-value car, comprehensive and collision coverage might be more important. For older cars with lower values, you might consider skipping these coverages to save on premiums.

Tip 5: Assess Your Risk Tolerance:

Your personal risk tolerance plays a role in choosing your coverage. If you prefer more financial protection and peace of mind, opting for higher coverage limits and additional coverage types may be suitable.

Tip 6: Shop Around for Competitive Rates:

Insurance premiums can vary significantly among providers. Take the time to shop around, obtain quotes from multiple insurers, and compare coverage options. Consider factors beyond price, such as customer service and claims satisfaction.

Tip 7: Bundle Policies for Discounts:

Many insurance companies offer discounts if you bundle multiple policies, such as auto and homeowners insurance. Bundling can result in cost savings, so inquire about available discounts when obtaining quotes.

Tip 8: Maintain a Good Driving Record:

A clean driving record can positively impact your insurance premiums. Safe driving habits and avoiding accidents and traffic violations can lead to lower rates and potential discounts.

Tip 9: Understand Deductibles and Premiums:

Deductibles are the amount you pay out of pocket before your insurance coverage kicks in. Choosing a higher deductible can lower your premiums but increases the amount you pay in the event of a claim. Find a balance that aligns with your budget.

Tip 10: Review and Update Your Policy Regularly:

Life changes, and so do your insurance needs. Regularly review and update your policy to ensure it reflects your current situation. Factors such as changes in vehicles, drivers, or address can impact your coverage requirements.

Tip 11: Utilize Discounts for Safe Driving Habits:

Many insurers offer discounts for safe driving habits. Consider participating in programs that track your driving behavior using telematics devices. Safe driving can lead to additional savings on your premiums.

Tip 12: Understand Policy Exclusions and Limitations:

Familiarize yourself with the exclusions and limitations of your policy. Certain situations, such as using your vehicle for commercial purposes or intentional acts, may not be covered. Knowing these exclusions can help you avoid surprises when filing a claim.

Tip 13: Consider Gap Insurance for New Vehicles:

If you’re financing or leasing a new vehicle, consider adding gap insurance. This coverage pays the difference between the actual cash value of your vehicle and the amount you owe on your loan or lease if it’s totaled.

Tip 14: Be Informed About No-fault Insurance:

Some states follow a no-fault insurance system, where each driver’s insurance covers their medical expenses and other losses, regardless of fault. Understand the implications of no-fault insurance in your state.

Tip 15: Seek Professional Advice When Needed:

If you find the process overwhelming or have specific questions, don’t hesitate to seek advice from an insurance professional or broker. They can provide guidance tailored to your situation and help you understand complex policy details.

Conclusion:

Choosing the right auto insurance coverage requires a thoughtful and informed approach. By understanding your needs, evaluating coverage options, and being proactive in managing your policy, you can ensure that you have the protection you need on the road. Regular reviews, safe driving habits, and staying informed about potential discounts and coverage options will contribute to a well-rounded and cost-effective auto insurance strategy.